Back to Blog

Back to Blog

You know the golden rule of running a business: keep personal and business finances separate. But sometimes, despite your best efforts, it’s tough to keep them apart – and business credit cards are a prime example. When you’re applying for one, chances are you’ll need to share your personal credit history. It’s all part of the game, especially when you’re just starting out.

Because let’s face it, without an established credit history for your business, you might have to sign a personal guarantee, making you personally responsible for any business debts. Business credit cards can be a lifesaver for keeping things running smoothly, but they do come with their fair share of risks. From high processing fees to security concerns and long processing times, it’s essential to use them wisely.

The role of personal credit in business credit card approval

When card issuers approve credit card applications, their primary decision factor is risk. Before extending credit, they want to know if, historically, a borrower has paid back their obligations on time. The tricky issue for new businesses is their lack of credit history. It’s hard to determine how good you are at paying off debt if your company doesn’t have a borrowing history in the first place. This forces creditors to look elsewhere to get a sense of their applicants’ creditworthiness. The first place they look? Your personal credit.

If an applicant has a personal history of paying on time, they’ll likely pay their business credit card bills on time too. In this respect, business credit cards function as an extension of your credit. Until your business takes on debts of its own and builds its business credit history, your track record serves as a substitute.

Personal guarantees & business credit cards

The connection between personal credit and business credit cards doesn’t end at the application process. You can expect to sign a personal guarantee when you open your card as well. The personal guarantee is a promise to your creditor that you will pay for debts if your business can’t.

The idea of taking on your business debt can sound intimidating. After all, most entrepreneurs set up business entities like limited liability corporations (LLCs) or S-corps to separate their business liability from their obligations. But business entities only offer so much protection and little of it extends to paying off your company’s credit card balance.

The CARD Act of 2009 protects personal credit card holders from several practices, such as arbitrary interest rate increases, double-cycle billing, and unfair payment allocations. But the act doesn’t cover business credit cards. Many major business credit card providers offer their customers the same or similar protection. When you apply for a card, just make sure you know if your provider offers any protection from unfriendly practices.

Why avoiding personal guarantees can be challenging?

Not every credit card requires a personal liability guarantee. There’s a chance you won’t have to sign one if your personal credit is stellar, you have a preexisting relationship with your creditor, or your business already has a solid credit history. Alternatively, you and your business partners can apply for a limited liability business credit card, but unless you’re making millions in revenue, you probably won’t get approval.

Regardless, unless you specifically go out of your way to avoid a personal guarantee on your business credit card — and have an outstanding credit history with significant revenue — you’re likely going to need to sign one.

How does business debt affect personal debt?

Not only are you personally responsible for business credit card debts if your company can’t take care of them — your personal credit history will also be on the line if creditors don’t get paid. Of course, bankruptcy is a last resort. If your company completes the Chapter 11 process, you can still potentially continue to run your business and settle your debts entirely through the financial veil of your company.

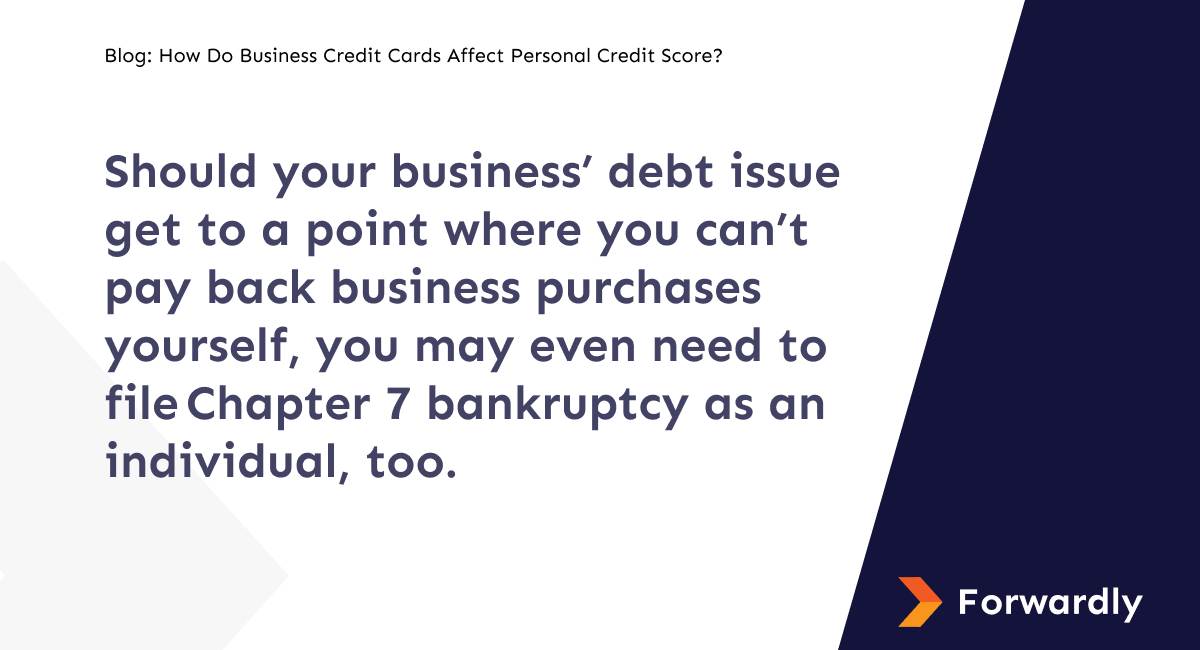

But, if your company doesn’t qualify, can’t meet obligations, or otherwise folds before or after bankruptcy — you’re personally liable for your company’s unpaid credit card bills. Should your business’ debt issue get to a point where you can’t pay back business purchases yourself, you may even need to file Chapter 7 bankruptcy as an individual, too.

Protecting your business and personal credit

Protecting your business and personal credit is crucial, and it’s understandable to feel uneasy about business credit card providers having access to your personal finances. But don’t worry, there are ways to minimize this risk.

One key strategy is to build a solid credit history for your business. The longer you consistently pay on time, the more trustworthy you’ll appear to creditors, which can lead to better interest rates and more flexibility in payment terms. Plus, as your business matures over time, banks are more likely to see your business’s financials separately from your personal history. It’s a waiting game, but patience pays off.

Remember, relying solely on business credit cards for business payments may not be the best choice financially, as they often come with high processing fees and slow transaction processing times. Consider switching to cost effective instant payments and same-day ACH payments, like those offered by Forwardly, to save money and streamline your cash flow. With Forwardly’s free cash flow forecasting tool, you can get a clear picture of your finances and make informed decisions to protect your business and personal credit.

Don’t let financial worries hold you back – start protecting your business and personal credit today with Forwardly!