Back to Blog

Back to Blog

The way we handle money in 2023 has changed a lot thanks to the rise of financial technology since the pandemic. Three modern ways that money moves around these days are through Automated Clearing House (ACH) payments, instant payments, and credit cards. These methods offer lots of benefits like being quick, easy, and efficient, which is why businesses and consumers love using them. But as we embrace these digital ways of paying, it’s super important to think about how to keep our money safe. That’s what this guide is all about – we’ll dig into payment security, identify potential risks, and provide strategies to safeguard your business from fraud.

Understanding ACH benefits and risks

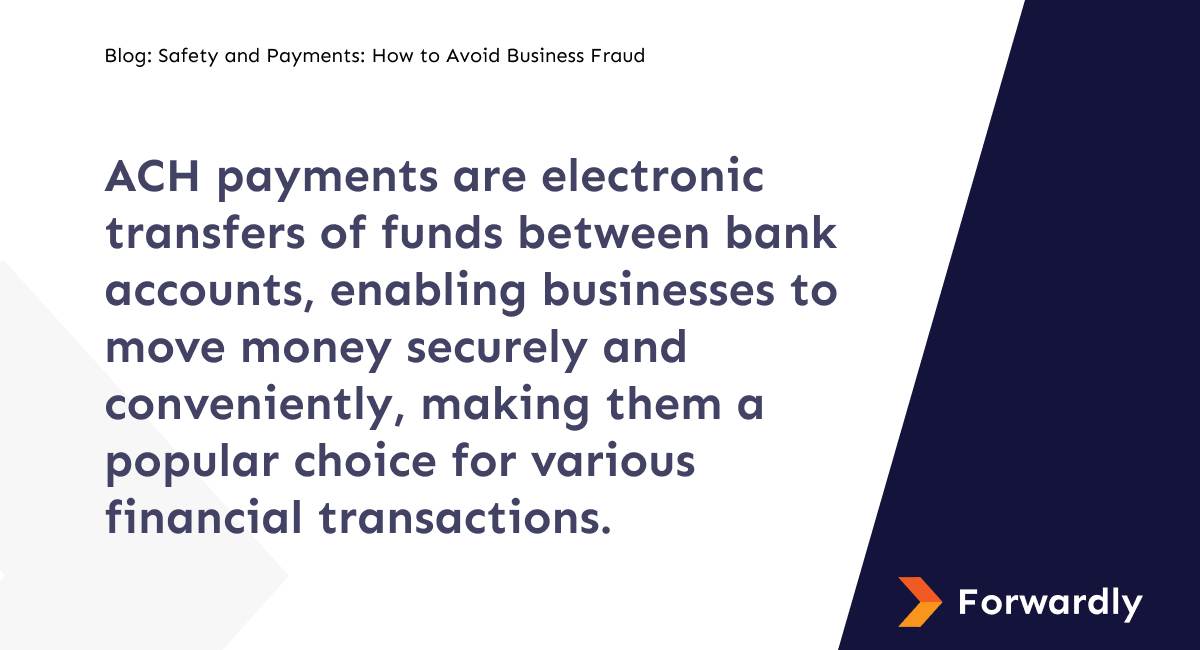

ACH payments are electronic transfers of funds between bank accounts. They enable businesses to move money securely and conveniently, making them a popular choice for various financial transactions. ACH payments are commonly used for activities like payroll direct deposits, bill payments, and recurring transactions.

According to the 2022 survey, a significant majority of respondents, specifically 87%, indicated their acceptance of ACH credit transactions for incoming payments. Additionally, 73% of respondents reported accepting ACH debit transactions for incoming payments. Furthermore, 78% of the surveyed participants reported using either ACH credit or ACH debit transactions for outgoing payments. So, it’s safe to say ACH transfers have become a go-to for business owners even though it’s one of the slowest payment options.

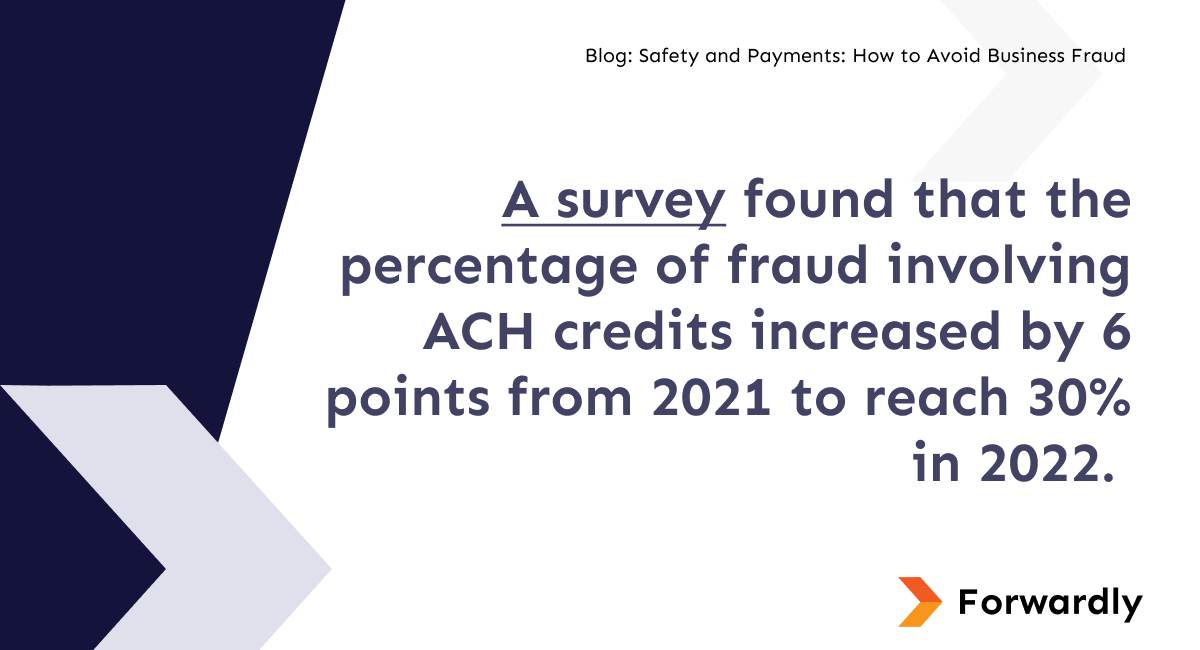

The benefits of ACH payments include cost-effectiveness, faster processing times compared to traditional paper checks, and improved cash flow management. However, using the ACH system for money transactions has some risks, like unauthorized payments and scams that can harm your financial safety. A survey found that the percentage of fraud involving ACH credits increased by 6 points from 2021 to reach 30% in 2022.

ACH business fraud occurs when someone steals money using this system. To pull it off, they need two things: your bank account number and your bank’s routing number. Armed with these, they can withdraw money from your account all at once or in small bits over time. They can also make payments without your permission. The issue with ACH transactions is that they don’t happen instantly, which gives dishonest individuals a chance to exploit this delay.

Instant payments: Efficiency and risks

Instant payments have gained popularity due to their speed and efficiency. They allow for near-instantaneous money transfers, reducing transaction times and enabling real-time financial transactions. The new FedNow Service has made instant payments even more well-known. The growing rise of faster payment technology makes it easier and more convenient for both businesses and individuals to use instant payments.

While instant payments offer efficiency, they are not without risks. Fraudsters may exploit the speed of instant transactions to their advantage. Understanding these risks is important for safeguarding your business against fraudulent activities.

Phishing: Fraudsters use emails, calls, or fake websites to trick individuals into revealing personal info. Educate customers about phishing risks through awareness campaigns to complement bank fraud prevention efforts.

APP Fraud: This happens when customers are deceived into sending money to a criminal’s account. To prevent this, perform thorough customer checks during onboarding and regularly review their spending habits. You can also use AI for monitoring.

ATO (Account Takeover) Attacks: In ATO attacks, fraudsters use stolen information to access bank accounts. Implement a rules-based system to detect unusual activity. Collaborate with a computer security incident response team (CSIRT) to address wider cybersecurity threats.

Credit card transactions: A common target

Credit card transactions are a common and integral part of business payments. Even though credit cards have high processing fees, they continue to be one of the favourite payment methods for businesses. They provide flexibility for customers and businesses alike, facilitating easy payments.

Because of their convenience, credit card transactions are often a target for fraudsters. Around 46% of global credit card frauds occur in the United States. Common types of credit card business fraud include card-not-present fraud, card-present fraud, and identity theft. According to a survey, the number of organizations that experienced fraud attacks through corporate/commercial credit cards increased from 26% to 36% in 2022. It’s essential to be vigilant and proactive in detecting and preventing credit card fraud.

Lost or Stolen Credit Cards: Fraudsters gain access to your credit card information by either taking your physical credit card or obtaining the card details after it’s lost or stolen. They can then use this information for unauthorized transactions.

Skimming Your Credit Card: Credit card skimming involves criminals placing hidden devices on card readers, like those found at gas station pumps. These devices capture card information when customers swipe their cards, allowing fraudsters to steal this data for illicit purposes.

Hacking Your Computer: Cybercriminals may use various hacking techniques to infiltrate your computer and access sensitive information, including credit card details stored on your device. These breaches can lead to identity theft and financial fraud.

Calling About Fake Prizes or Wire Transfers: Fraudsters often employ phone scams where they impersonate legitimate organizations, claiming you’ve won prizes or need to initiate wire transfers. Unsuspecting victims may divulge personal and financial information, falling victim to these scams.

Phishing Attempts: Phishing involves sending deceptive emails that appear to be from reputable sources. These emails aim to trick recipients into revealing personal and financial information. Clicking on malicious links or sharing sensitive data can lead to fraud.

Stealing Your Mail: Thieves may steal your mail, including credit card statements, new credit cards, or sensitive documents. By intercepting your mail, they can gain access to valuable information and potentially commit identity theft or credit card fraud.

Strategies to protect your business

Keeping your finances safe from business fraud isn’t just about staying safe; it’s like having a strong foundation of trust and strength. In our world today, everything is becoming digital, and it’s easy for money and important information to be at risk with just a few clicks. That’s why we really need to focus on making sure our security is tough and can handle all the challenges that might come our way.

Strengthening account security: Implementing robust security measures for your business accounts is essential to safeguard sensitive financial data. Start by enforcing strong password policies and regular changes. Employ role-based access control to limit access to critical systems and data. Utilize password management tools to securely store and manage login credentials. These measures will create a robust defense against unauthorized access and potential breaches.

Implementing robust verification procedures: To ensure the authenticity of transactions and payment requests, it’s crucial to establish robust verification procedures. Use encrypted and authenticated communication channels for transaction verification. Consider implementing digital signatures and encryption to secure transaction data. Implement a clear approval process, especially for high-value transactions, that requires multiple levels of authorization, reducing the risk of unauthorized transfers.

Educating employees: Your staff can be your first line of defense against financial fraud. Comprehensive training on recognizing common fraud schemes is vital. Ensure they are aware of phishing, social engineering, and invoice fraud tactics.

Monitoring transactions: To detect any anomalies or unauthorized activities, regular transaction monitoring is essential. Utilize automated tools to flag unusual or potentially fraudulent transactions. Set up real-time alerts for large or suspicious activities

Using secure payment gateways: Selecting a reputable and secure payment gateway is fundamental for processing online payments safely. Research and choose payment processors that comply with industry security standards. Ensure that the chosen gateway supports encryption and tokenization for safeguarding sensitive financial data.

Regularly updating software: Keeping your payment processing software, operating systems, and antivirus solutions up to date is a cornerstone of financial security. Apply patches and updates promptly to protect against known vulnerabilities.

Verifying customer identity: In high-value transactions, verifying the identity of customers is crucial. Implement know-your-customer (KYC) procedures to confirm the authenticity of customer information. Use identity verification tools and databases to validate customer identities.

Moving Forwardly with safety in mind

In a world where the way we handle payments continues to evolve, understanding and prioritizing payment security is crucial. ACH payments, instant payments, and credit cards each come with their unique advantages and risks. By recognizing potential fraud risks, implementing security measures, and staying vigilant, you can protect your business’s financial integrity and reputation.

But what if there was a solution that could not only simplify your payment processes but also provide top-notch security? That’s where Forwardly comes into the picture.

Forwardly provides safe and secure instant payments and same-day ACH that doesn’t require trading banking details. Beyond its robust security measures, Forwardly’s commitment to industry regulations and best practices reinforces its stance as a trusted provider. The platform adheres to NACHA rules and utilizes the advanced ISO20022 standard for instant payments, offering structured and rich data for better security.

With Forwardly, you can enjoy the convenience of modern payment methods without compromising on security. As the financial landscape continues to evolve, having a trusted partner like Forwardly can make all the difference in safeguarding your business from payment fraud. It’s time to embrace innovation and security hand in hand for a more confident and secure financial future. Sign up today!