Back to Blog

Back to Blog

Originally Published on Forbes.

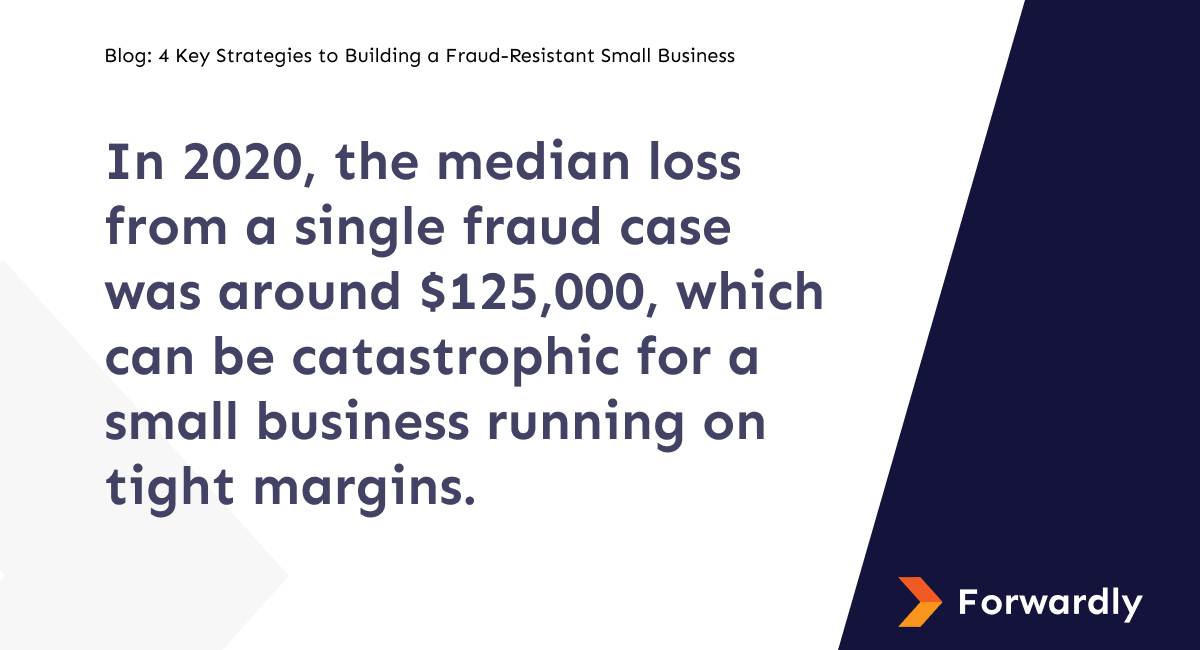

Fraud is a significant threat to small businesses, causing them to lose about 5% of their annual revenue, according to the Association of Certified Fraud Examiners (ACFE). It’s not just about the financial loss; fraud also undermines a business’s stability and reputation in the market. In 2020, the median loss from a single fraud case was around $125,000, which can be catastrophic for a small business running on tight margins. Phishing, malware, internal fraud, check fraud, and credit card scams are all common types of fraud that small businesses encounter.

These fraudulent activities can have a far-reaching impact, affecting not only your finances but also your reputation and trust among stakeholders. To protect your business, you can adopt four strategies tailored to your specific needs and circumstances. While no business is entirely immune to fraud, implementing robust defenses is essential to safeguarding your business and its assets.

Strategy 1: Implement robust internal controls

For small businesses to prevent fraud effectively, it’s crucial to have strong internal controls in place. These controls include clear rules, regular checks, and keeping an eye on things. With internal theft being a big concern for two-thirds of small businesses according to the National Federation of Independent Business— implementing specific rules like segregating duties and enforcing mandatory authorization processes for financial transactions can be highly effective. Segregating duties ensures no single individual has sole control, reducing the risk of fraud. Dual authorization adds an extra layer of scrutiny, minimizing the chance of unauthorized activities.

Using advanced technology like machine learning and AI can help catch fraud early. A recent report by Fortune Business Insights found that companies spend over $11 billion to use technology against fraud. Regular fraud checks are essential. Business leaders should meticulously review financial records, transaction logs, and employee access. Paying attention to any discrepancies or anomalies can help detect fraudulent activities early. Surprise audits and rotating responsibilities can also deter potential fraudsters and uncover irregularities.

By maintaining clear rules, conducting routine checks, and providing comprehensive staff training, small businesses can mitigate risks. These measures not only safeguard finances but also uphold the business’s integrity and reputation.

Strategy 2: Educate your employees

Your employees are crucial in protecting your business from fraud. Educating them about fraud prevention not only raises awareness of potential risks but also empowers them to spot and report suspicious activities effectively. According to the ACFE, employee tips are the most common way fraud is detected, making up nearly 43% of all cases. Having clear written guidelines outlining the company’s fraud prevention rules and encouraging a culture of staying alert further strengthens the business’s defences against fraud.

Businesses need to make sure employees know how to recognize and respond to fraud threats. Training sessions should cover things like how to spot phishing emails and how to keep passwords safe to prevent unauthorized access to sensitive information. Employees should be kept up to date on the latest fraud schemes through regular updates from management. Having clear company policies in place helps employees know what to do and ensures everyone follows the best practices. By investing in educating employees and having strong fraud prevention measures, businesses can reduce the risk of fraud and protect themselves effectively.

Strategy 3: Securing online financial transactions

As digital transactions become more common, small businesses need to protect their financial processes from fraud. This means taking steps to protect sensitive financial information and transactions from being tampered with or accessed by unauthorized people. According to Javelin Strategy & Research, fraudsters caused $56 billion in losses in 2020, mainly through identity theft and taking over accounts.

To secure financial transactions, consider utilizing encryption technologies to protect data transmitted over digital channels and partnering with reputable payment processors for secure online transactions. Implementing multi-factor authentication mechanisms, like biometric verification, adds an extra layer of security by verifying user identities and preventing unauthorized access to financial accounts. And don’t forget to look for modern payment solutions that focus on security to give your accounts payable and accounts receivable process an extra layer of protection. By adopting these measures, small business owners can improve the integrity of their financial transactions and reduce the risk of fraud-related losses.

Strategy 4: Invest in insurance

Despite meticulous preventive measures, the risk of fraud can never be entirely eliminated. That’s where insurance steps in as a safety net, providing financial protection if fraud impacts our business. With organizations losing an average of 5% of their revenue to fraud each year, and US financial institutions facing an estimated $4.2 billion in fraud costs in 2021 alone, having insurance is a wise decision for small business owners.

Whether it’s theft or cyber-attacks, insurance helps us recover from losses caused by fraudulent activities. Policies like crime insurance, cyber liability insurance, and fidelity bonds offer tailored protections against various fraud-related risks.

Crime insurance is invaluable for covering losses stemming from theft, forgery, and fraud, providing much-needed financial reimbursement. Cyber liability insurance is essential in safeguarding against losses resulting from cyber threats such as data breaches and ransomware attacks. Meanwhile, fidelity bonds offer protection against employee dishonesty, ensuring businesses are reimbursed for losses caused by fraudulent acts committed by the staff.

Despite the ongoing risk of fraud, small business owners need to stay alert and adaptable. Having a solid plan to tackle fraud, which includes strong rules, educating employees, securing financial transactions, and having insurance, makes our businesses more resilient to evolving threats. Clear rules, dividing tasks, and regular checks help reduce vulnerabilities. Staying updated on new fraud methods and reviewing our prevention plan regularly is crucial. With these steps, we can safeguard our businesses and ensure their long-term success.